Time collection evaluation is broadly used for forecasting and predicting future factors in a time collection. AutoRegressive Built-in Transferring Common (ARIMA) fashions are broadly used for time collection forecasting and are thought-about one of the crucial well-liked approaches. On this tutorial, we are going to learn to construct and consider ARIMA fashions for time collection forecasting in Python.

Our Prime 5 Free Course Suggestions

What’s an ARIMA Mannequin?

The ARIMA mannequin is a statistical mannequin utilized for analyzing and predicting time collection information. The ARIMA method explicitly caters to straightforward buildings present in time collection, offering a easy but highly effective technique for making skillful time collection forecasts.

ARIMA stands for AutoRegressive Built-in Transferring Common. It combines three key points:

- Autoregression (AR): A mannequin that makes use of the correlation between the present remark and lagged observations. The variety of lagged observations is known as the lag order or p.

- Built-in (I): Using differencing of uncooked observations to make the time collection stationary. The variety of differencing operations is known as d.

- Transferring Common (MA): A mannequin takes under consideration the connection between the present remark and the residual errors from a shifting common mannequin utilized to previous observations. The scale of the shifting common window is the order or q.

The ARIMA mannequin is outlined with the notation ARIMA(p,d,q) the place p, d, and q are substituted with integer values to specify the precise mannequin getting used.

Key assumptions when adopting an ARIMA mannequin:

- The time collection was generated from an underlying ARIMA course of.

- The parameters p, d, q have to be appropriately specified based mostly on the uncooked observations.

- The time collection information have to be made stationary through differencing earlier than becoming the ARIMA mannequin.

- The residuals must be uncorrelated and usually distributed if the mannequin matches effectively.

In abstract, the ARIMA mannequin gives a structured and configurable method for modeling time collection information for functions like forecasting. Subsequent we are going to take a look at becoming ARIMA fashions in Python.

Python Code Instance

On this tutorial, we are going to use Netflix Inventory Information from Kaggle to forecast the Netflix inventory value utilizing the ARIMA mannequin.

Information Loading

We are going to load our inventory value dataset with the “Date” column as index.

import pandas as pd

net_df = pd.read_csv("Netflix_stock_history.csv", index_col="Date", parse_dates=True)

net_df.head(3)

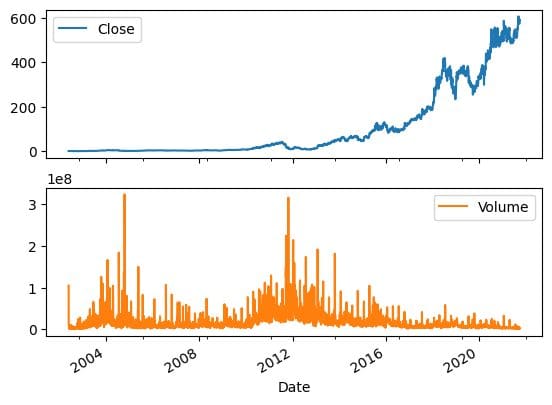

Information Visualization

We will use pandas ‘plot’ operate to visualise the adjustments in inventory value and quantity over time. It is clear that the inventory costs are growing exponentially.

net_df[["Close","Volume"]].plot(subplots=True, format=(2,1));

Rolling Forecast ARIMA Mannequin

Our dataset has been cut up into coaching and take a look at units, and we proceeded to coach an ARIMA mannequin. The primary prediction was then forecasted.

We obtained a poor consequence with the generic ARIMA mannequin, because it produced a flat line. Subsequently, we’ve got determined to attempt a rolling forecast technique.

Notice: The code instance is a modified model of the pocket book by BOGDAN IVANYUK.

from statsmodels.tsa.arima.mannequin import ARIMA

from sklearn.metrics import mean_squared_error, mean_absolute_error

import math

train_data, test_data = net_df[0:int(len(net_df)*0.9)], net_df[int(len(net_df)*0.9):]

train_arima = train_data['Open']

test_arima = test_data['Open']

historical past = [x for x in train_arima]

y = test_arima

# make first prediction

predictions = checklist()

mannequin = ARIMA(historical past, order=(1,1,0))

model_fit = mannequin.match()

yhat = model_fit.forecast()[0]

predictions.append(yhat)

historical past.append(y[0])

When coping with time collection information, a rolling forecast is usually mandatory as a result of dependence on prior observations. A technique to do that is to re-create the mannequin after every new remark is obtained.

To maintain monitor of all observations, we are able to manually keep a listing known as historical past, which initially comprises coaching information and to which new observations are appended every iteration. This method might help us get an correct forecasting mannequin.

# rolling forecasts

for i in vary(1, len(y)):

# predict

mannequin = ARIMA(historical past, order=(1,1,0))

model_fit = mannequin.match()

yhat = model_fit.forecast()[0]

# invert remodeled prediction

predictions.append(yhat)

# remark

obs = y[i]

historical past.append(obs)

Mannequin Analysis

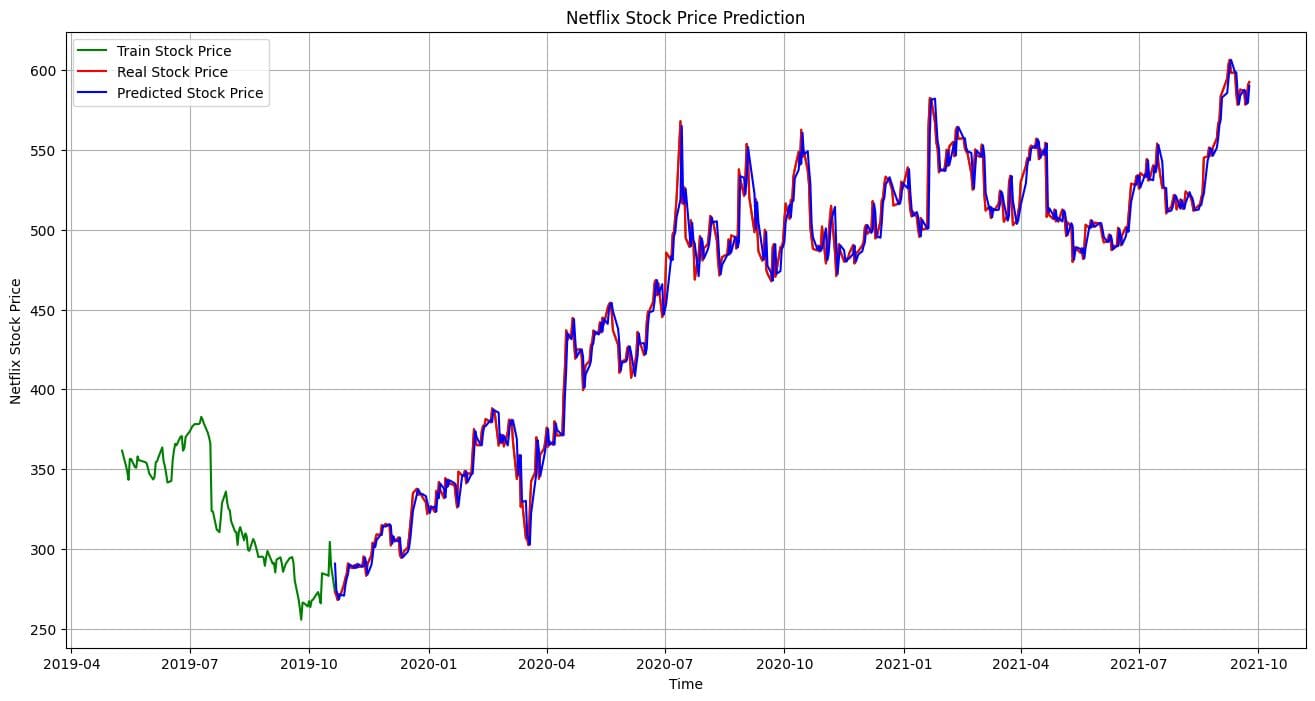

Our rolling forecast ARIMA mannequin confirmed a 100% enchancment over easy implementation, yielding spectacular outcomes.

# report efficiency

mse = mean_squared_error(y, predictions)

print('MSE: '+str(mse))

mae = mean_absolute_error(y, predictions)

print('MAE: '+str(mae))

rmse = math.sqrt(mean_squared_error(y, predictions))

print('RMSE: '+str(rmse))

MSE: 116.89611817706545

MAE: 7.690948135967959

RMSE: 10.811850821069696

Let’s visualize and evaluate the precise outcomes to the anticipated ones . It is clear that our mannequin has made extremely correct predictions.

import matplotlib.pyplot as plt

plt.determine(figsize=(16,8))

plt.plot(net_df.index[-600:], net_df['Open'].tail(600), shade='inexperienced', label = 'Prepare Inventory Value')

plt.plot(test_data.index, y, shade = 'pink', label = 'Actual Inventory Value')

plt.plot(test_data.index, predictions, shade = 'blue', label = 'Predicted Inventory Value')

plt.title('Netflix Inventory Value Prediction')

plt.xlabel('Time')

plt.ylabel('Netflix Inventory Value')

plt.legend()

plt.grid(True)

plt.savefig('arima_model.pdf')

plt.present()

Conclusion

On this quick tutorial, we offered an summary of ARIMA fashions and the way to implement them in Python for time collection forecasting. The ARIMA method gives a versatile and structured strategy to mannequin time collection information that depends on prior observations in addition to previous prediction errors. If you happen to’re curious about a complete evaluation of the ARIMA mannequin and Time Sequence evaluation, I like to recommend having a look at Inventory Market Forecasting Utilizing Time Sequence Evaluation.